The latest foreign direct investment (FDI) data showed that global FDI inflows dropped by 2 per cent in 2023 to a total of US$1.33 trillion, while ASEAN saw record inflows for the third year with a gain of 1.2 per cent to US$226.3 billion.

Robust economic growth and extensive global value chain (GVC) linkages have contributed to ASEAN’s performance. Singapore remained the largest FDI destination, rising 13 per cent to nearly US$160 billion, while Vietnam gained 3.4 per cent to US$18.5 billion.

In terms of outlook, a greater degree of cross-border coordination, deepening integration, political stability, and demographic dividend in ASEAN will be supportive of positive prospects ahead.

Record FDI inflows into ASEAN for the third year amid global declines

In the FDI data released late June 2024 by the United Nations Trade and Development (UNCTAD), the 10-member Southeast Asian grouping (ASEAN) remained the world’s top destination of FDI inflows in 2023 after the US, registering its third year of record inflows.

Global FDI inflows totaled US$1.33 trillion in 2023, a 2 per cent drop from 2022, which UNCTAD attributed to the “wild swings” in a small number of European conduit economies, partly due to the global minimum tax (GMT) for large multinational enterprises (MNEs) as well as “a big drop” in the value of cross-border M&As in developed markets. Excluding the effect of these conduits, the headline global FDI inflows in 2023 experienced a far larger decline, down by more than 10 per cent year-on-year, while inflows to developing markets shrank by 7 per cent, led by Developing Asia, the largest FDI recipient, which dropped by 8 per cent.

Singapore retains its role as a regional hub

Similar to the headline figure, FDI flows to Developing Asia receded in 2023 but remained elevated at US$621 billion, and the region stayed as the largest recipient of FDI, accounting for nearly half of global inflows.

While inflows declined in East Asia, due to a significant drop in China after a decade-long growth trend, inflows to ASEAN remained stable as a result of robust economic growth and extensive global value chain (GVC) linkages, as highlighted in the World Investment Report (WIR).

In Developing Asia, inflows to China fell by 14 per cent to US$163.3 billion, while those to India plunged 43 per cent year-on-year to US$28.2 billion. In contrast, inflows to ASEAN rose 1.2 per cent to US$226.3 billion in 2023, although the distributions were uneven, gripped by tight monetary policy conditions worldwide.

Among ASEAN members, Singapore remained the largest FDI destination, rising 13 per cent to nearly US$160 billion while Vietnam saw a smaller increase of 3.4 per cent to US$18.5 billion. However, Indonesia, Malaysia and Thailand reported year-on-year declines of 15 per cent to 59 per cent, following the broader global trends as economic activities slowed in response to tight monetary policy stance by various central banks.

The WIR noted that greenfield investments have been a main driving force during the year. The overall value and the number of greenfield project announcements in Developing Asia increased significantly by 44 per cent and 22 per cent respectively. In ASEAN, there was a 42 per cent year-on-year jump in investment announced in 2023, particularly in electronics and vehicle production. Within ASEAN, Indonesia was a top destination for announced greenfield projects by value in 2023 (+73 per cent year-on-year), with notable investments including a glass and solar manufacturing project and battery supply chain for electric vehicles. Malaysia, the Philippines, Thailand and Vietnam also saw sharp increases in announced greenfield investment projects, with year-on-year gains of 49 per cent, 33 per cent, 88 per cent and 72 per cent, respectively.

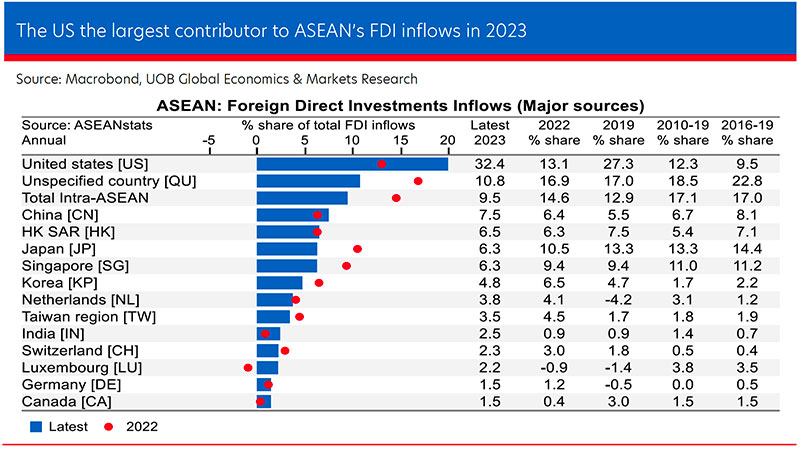

US remains the largest source of inflows to ASEAN

The US accounted for 32 per cent share of total inflows to ASEAN in 2023, more than double the 13 per cent share in 2022 and the average value of 12 per cent in 2010-2019, suggesting that rising US-China tensions, the shifting of supply chains and derisking/”friend-shoring” continue to be the main motivating factors.

Similar to the US but at a much smaller scale, inflows from Europe have increased significantly compared with the historical average. For example, inflows from Switzerland and Germany saw multiple times of increases compared with the 2010-2019 period.

In contrast, flows from China and Hong Kong SAR did not show significant deviations from its past growth trends. This suggests that in the boardrooms of these MNEs’ head offices, decisions are made to increase investments in locations such as ASEAN, while inflows to China and HK SAR saw a steady deceleration especially over the past few years.

Similar to past years, the financial services (42 per cent) and manufacturing (23 per cent) sectors remained the top two FDI recipients in 2023 (2022: 27 per cent and 33 per cent). Of note is that professional/technical services saw its share of FDI rising to 9.5 per cent from 0.1 per cent in 2022, a trend that is also highlighted by UNCTAD.

Positive prospects for ASEAN with possible shifts in patterns

Are FDI inflows to ASEAN sustainable in the years ahead? And will the decline in key ASEAN markets (Indonesia, Malaysia and Thailand) reverse? We believe that the following are key factors supporting a positive outlook in the next three to five years:

Greater cross-border policy coordination and cooperation: A truly groundbreaking development is the signing of the MOU between the Singapore and Malaysia governments in January 2024 to implement the Johor-Singapore Special Economic Zone (JS-SEZ). An agreement could be signed in September, according to a Malaysian minister. This enlightened approach of economic cooperation reflects the progressive and pragmatic approach in these governments’ business and investment policy.

Prevalence of the ASEAN spirit and the deepening integration of regional economies: Besides the JS-SEZ, other recent developments like the entering into force of the Regional Comprehensive Economic Partnership (RCEP) in 2022, the sizeable intra-ASEAN flows of trade and FDI, and increased adoption of cross-border payments via QR and digital channels, reflect increased integration of the region.

Domestic political stability: Power transitions after recent elections in Indonesia, Malaysia and Thailand have been smooth and uneventful, demonstrating the increased maturity of these countries, which ensure policy continuity and stability in these key ASEAN members at least in the next 3-5 years.

Population: Demographic dividend will be unfolding in the years ahead as income rises and wealth increases for the large pool of young population.

From the standpoint of an investor, a place with a greater degree of economic integration and coordination, political stability and lower frictions (such as smoother movements of people, goods and services) would certainly be conducive to deployment of tens or even hundreds of millions of dollars’ worth of investment projects.

Specifically, UNCTAD has identified some major FDI investment trends in an April 2024 study:

Increasing FDI flows to services (more service-centric and asset light investment cross-border investment)

Deglobalisation of manufacturing (increased localisation of production by shrinking international components and reduced trade in intermediate inputs with the fragmentation of global value chains)

Diminishing role of FDI in China (declining share of China in global FDI suggests transition from globally integrated production networks to more domestically focused ones)

Fracturing trend in FDI along geopolitical lines (i.e. reduction in investment between “geopolitically distant” countries)

The sustainability imperative driving new FDI sectors (FDI in environmental technologies stands out as the main pocket of growth outside services)

The increasing concentration of FDI and marginalisation of developing countries (FDI is increasingly concentrated in developed and emerging economies)

The trends highlighted by UNCTAD mirror that of UOB's clients' investment and business activities across the region. For instance, there is a trend towards services-oriented activities such as logistics, warehousing and distribution, coupled with a heightened focus on sustainability practices. Additionally, there is heightened awareness and strategic planning regarding the potential repercussions of escalating US-China tensions, which may extend to third countries.

Overall, ASEAN remains a unique location for companies which are progressively able to localise their production capability and contents as supply chains evolve to become more robust and extensive, particularly in the areas of intermediate inputs within the electronics sector.

Nonetheless, the WIR cautioned that the global environment for international investment “remains challenging” in 2024, due to weakening growth prospects, economic fracturing trends, trade and geopolitical tensions, industrial policies and supply chain diversification that are reshaping FDI patterns, causing some MNEs to adopt a cautious approach to overseas expansion.

Geoeconomic fragmentation is also reshaping the landscape of global investment, with fragmenting trade networks, diverging regulatory environments and the reconfiguring of international supply chains creating both obstacles and isolated opportunities, with some countries benefiting from investments in global value chain-intensive manufacturing while others struggle to participate in the global economy. This is a clear reminder that governments and businesses will need to stay nimble and competitive in such an environment.

This article shall not be copied or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Suan Teck Kin

UOB

Suan Teck Kin joined UOB as an economist in 2006. In his current role as Executive Director in Global Economics and Markets Research, he is responsible for macroeconomic and foreign exchange research with a primary focus on China, Hong Kong SAR and Taiwan, and secondary coverage for the ASEAN region. As a member of the Research team, he presents the team’s market views regularly to the Bank’s management team and clients in Singapore and the region.

Teck Kin has more than 10 years of experience in macroeconomics and equity research. Fluent in English and Mandarin, Teck Kin is interviewed frequently by local and international print and broadcast media, as well as financial newswires on the economic and market outlook.