What does the ASEAN consumer think and feel about the economy? How has spending and financial behaviour changed? Get the latest highlights from the region’s barometer of consumer sentiments.

What does the ASEAN consumer think and feel about the economy? How has spending and financial behaviour changed? Get the latest highlights from the region’s barometer of consumer sentiments.

2 in 3 tech-savvy small businesses bullish on future growth

Digitally Connected

03 Mar 2022

4 mins read

You are now reading:

2 in 3 tech-savvy small businesses bullish on future growth

Key takeaways

67 per cent of small- and medium-sized enterprises (SMEs) that embraced digitalisation are optimistic about their 2022 business performance.

The professional services sector has been most aggressive in adopting technology tools with nine in 10 SMEs already on their digital journey.

Banks have a vital role to play in supporting the digitalisation of SMEs for sustainable future growth.

The global pandemic has made it clear for Singapore’s SMEs that digitalisation is a necessity, not an option.

In fact, SMEs that adopted digitalisation tend to be more optimistic about their business performance in 2022, according to the UOB SME Outlook Study 20221. The study interviewed 800 business owners and key executives of SMEs with less than S$100 million in revenue.

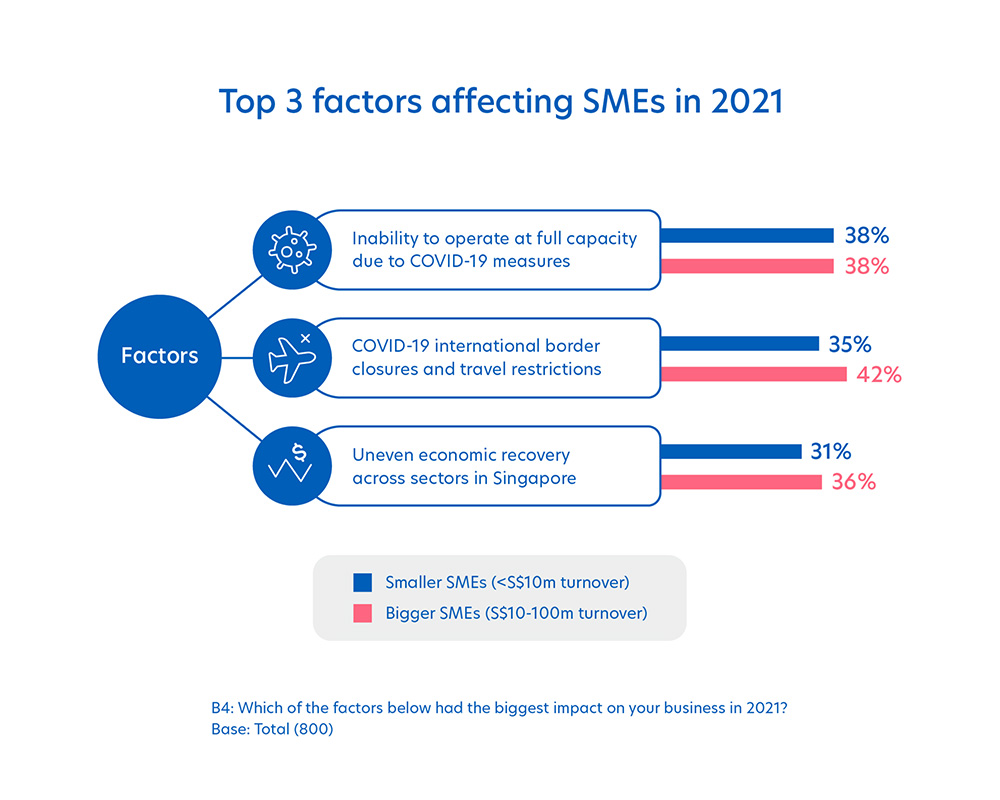

The impact of the COVID-19 pandemic was felt by all respondents, particularly those in the real estate, hospitality, community and personal services sectors.

Figure 1: Biggest factors that impacted SMEs in Singapore in 2021. Source: UOB SME Outlook Study 2022

Small businesses have always faced the pressure to build business resilience and stay competitive. However, those that have adopted digitalisation have shown an ability to withstand the economic turmoil from the last two years.

Among these businesses, 67 per cent saw success – with their business performance in 2022 labelled as ‘somewhat or vastly improving’. 27 per cent of the respondents who did not adopt digitalisation were not faring as well in 2021 and remained less optimistic about 2022 and beyond.

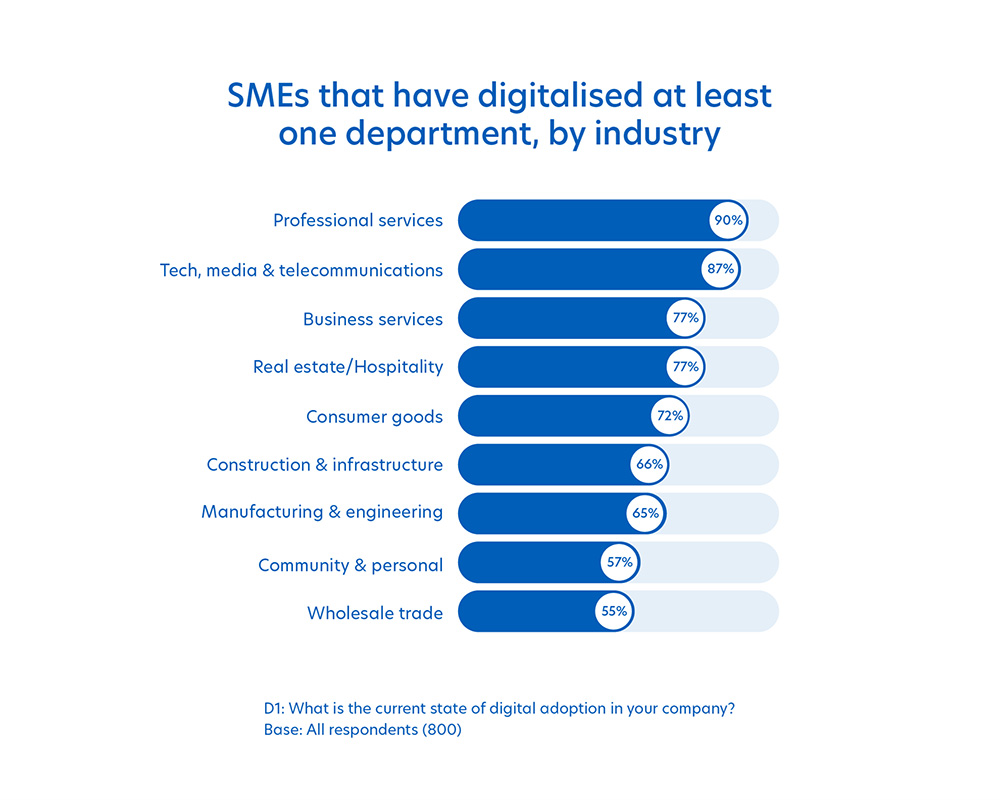

Professional services lead the charge

SMEs in the professional services sector had the highest level of digital adoption at 90 per cent of those interviewed. This may be because service processes can be digitalised more easily as compared to those within manufacturing and construction sectors. The technology, media and telecommunications sector came in second at 87 per cent.

Both the community and personal sector (57 per cent), as well as wholesale trade sector (55 per cent) had significantly lower digital adoption compared with the total sample.

Figure 2: Top industries that have embarked on digitalisation. Source: UOB SME Outlook Study 2022

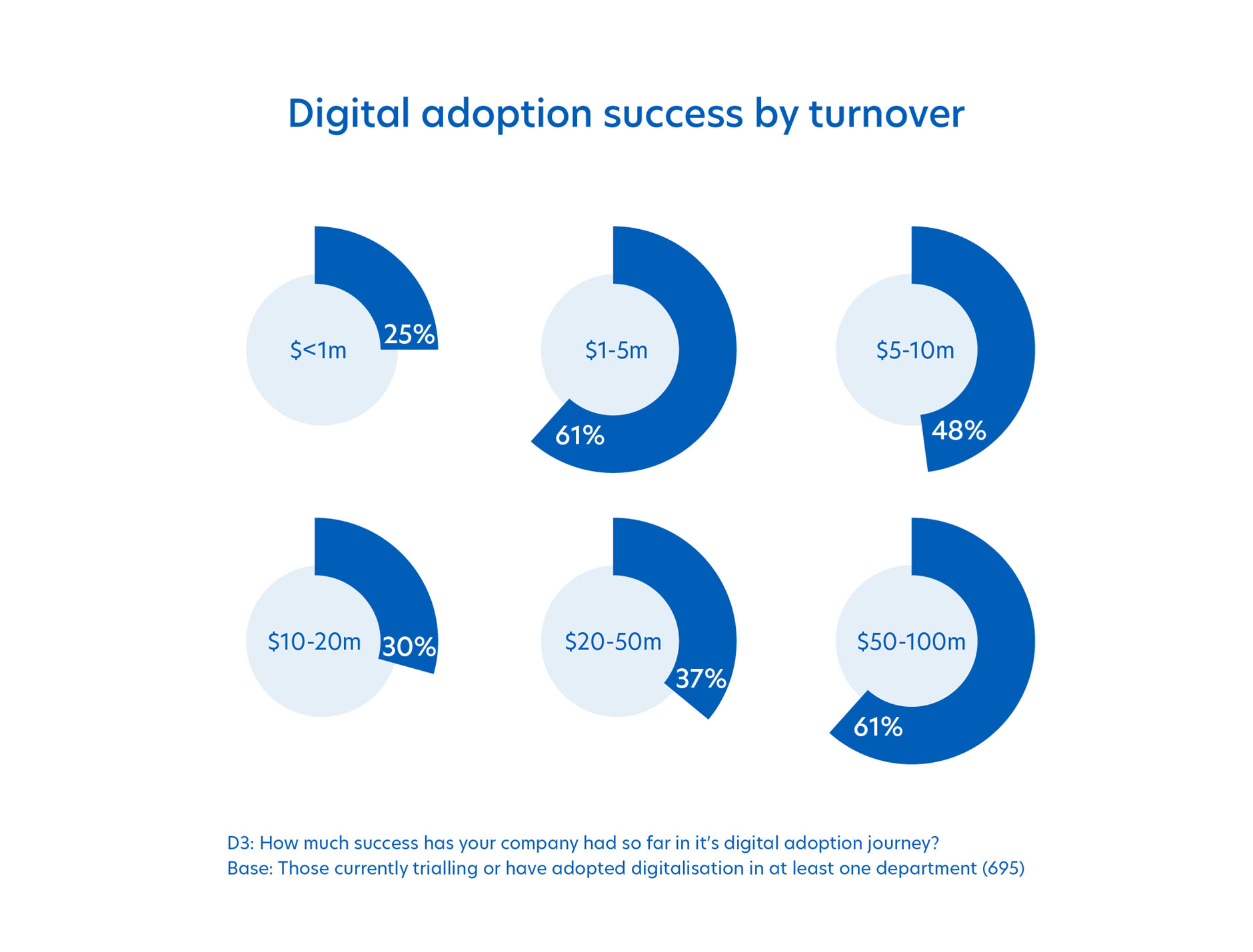

In terms of organisation size, SMEs with S$1-5 million and S$50-100 million in annual turnover fared better in their digitalisation journey.

For the smaller SMEs (S$1-5 million turnover), 61 per cent cited digital adoption success. They may have just started on their digitalisation journey and seen benefits such as better customer retention and competitive differentiation.

SMEs with S$50-100 million in annual turnover, on the other hand, are likely to have bigger budgets to leverage digitalisation more broadly across the organisation, and thus benefit from economies of scale due to lower IT infrastructure costs.

Figure 3: Digital adoption success by SMEs’ annual turnover. Source: UOB SME Outlook Study 2022

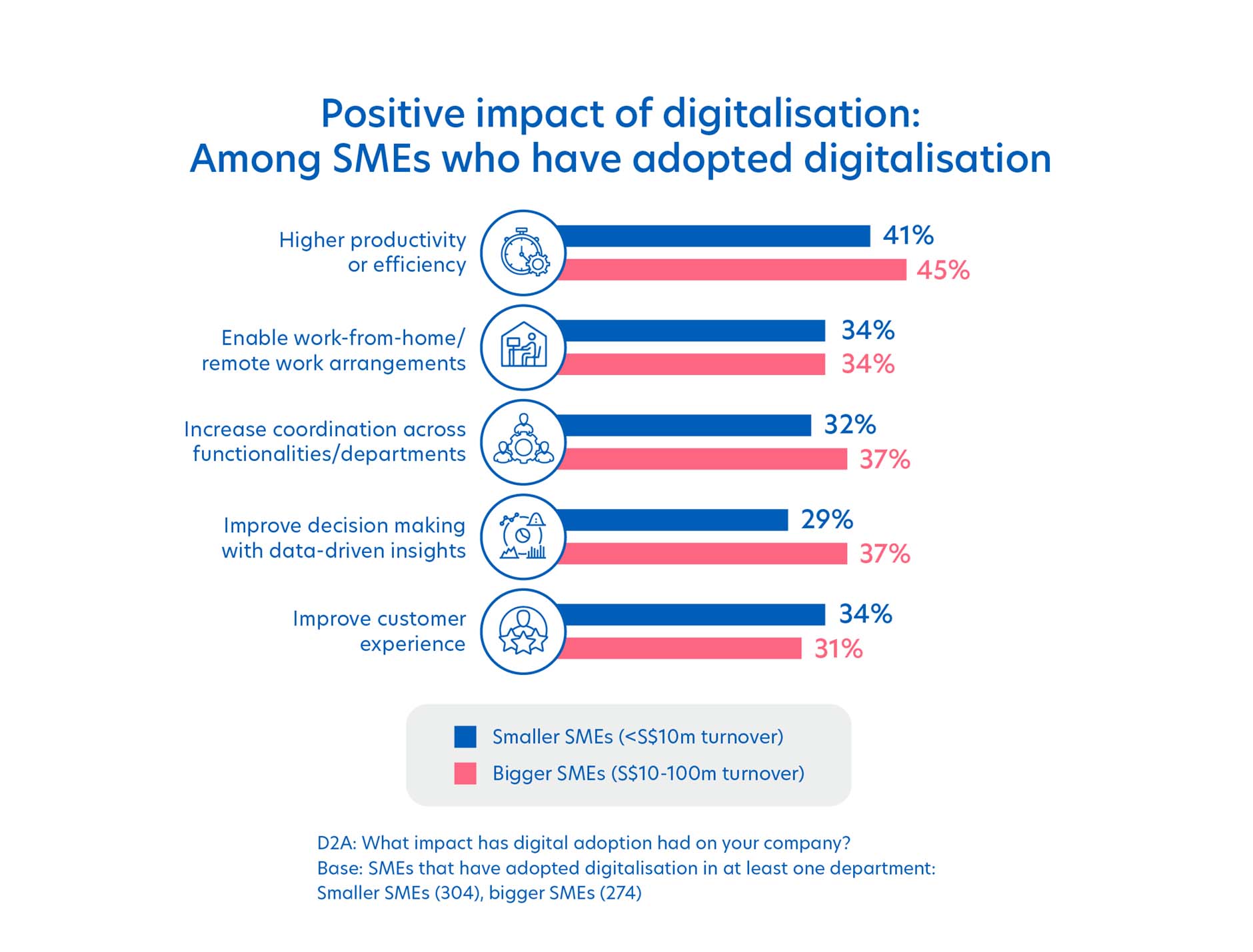

Productivity boost from embracing tech

Regardless of size, the biggest impact of digitalisation for SMEs has been higher productivity or efficiency. One in two SMEs with $10-100m turnover benefitted from this outcome.

The positive impact of digitalisation is particularly apparent among the bigger SMEs with S$10-$100m turnover. There was increased coordination across departments, improved decision-making with data-driven insights and overall higher productivity.

Even SMEs that have not started their digitalisation journey believe that doing so can have a positive impact on their business, from improving customer experience to improved decision-making with data-driven insights.

Figure 4: Top five areas of impact for digitalised SMEs. Source: UOB SME Outlook Study 2022

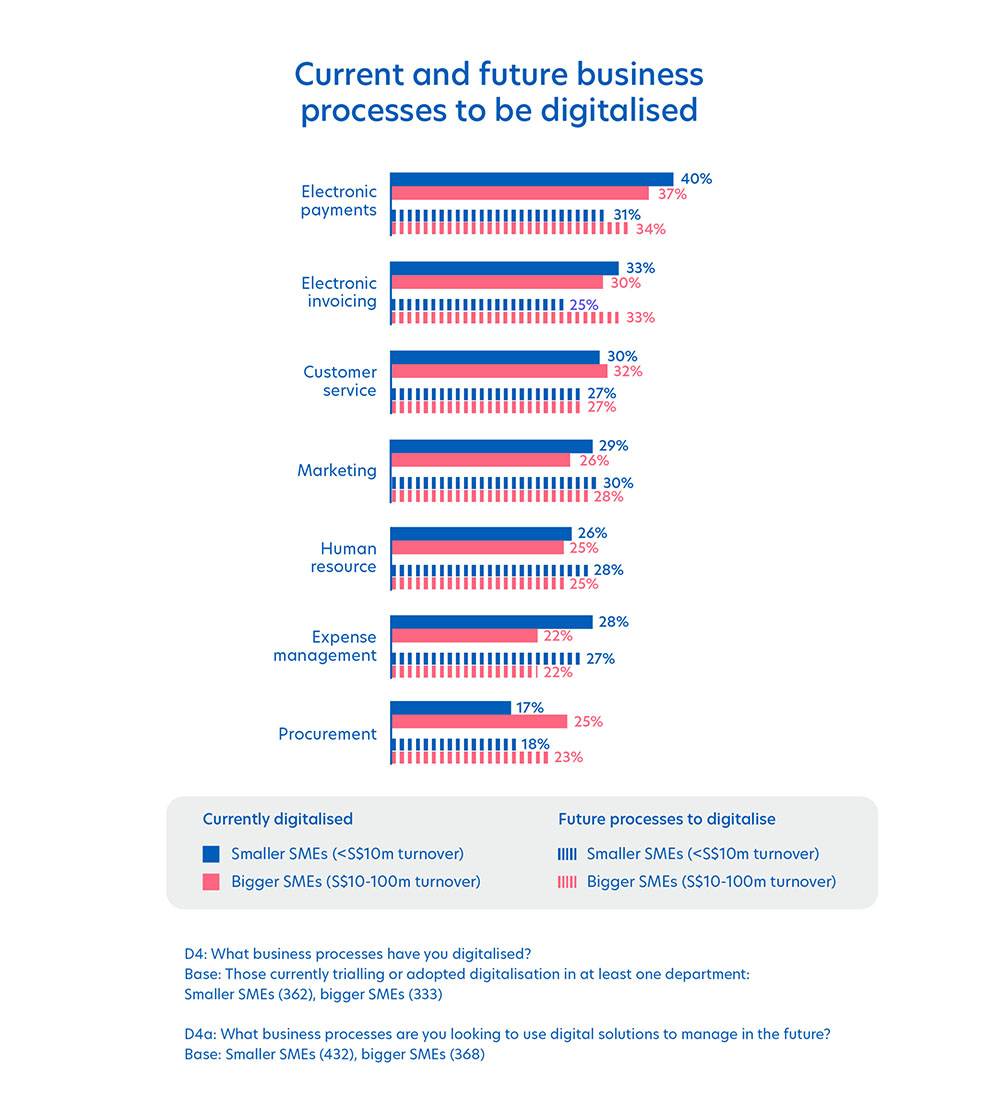

Tech focus on better customer engagement

Investments towards digitalisation tend to be customer-focused as SMEs prioritised electronic payments, electronic invoicing, customer service and marketing.

However, there is more work to be done in digitalising internal processes.

When reviewing future processes to digitalise, the respondents ranked human resource management (25 per cent), expense management (25 per cent) and procurement (21 per cent) as the lowest priority.

Figure 5: Current and future business processes to undergo digitalisation. Source: UOB SME Outlook Study 2022

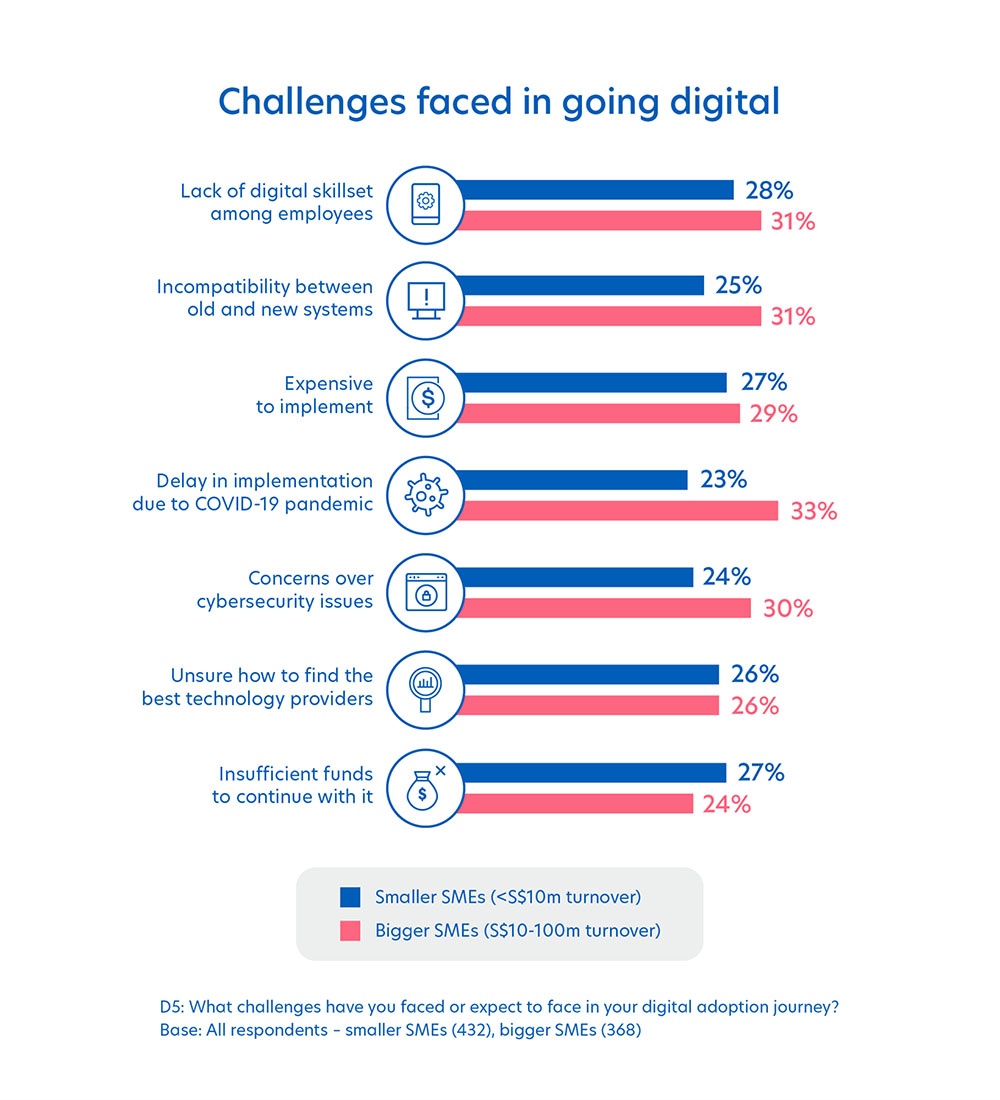

Lack of digital skillsets a major challenge

The path to digitalisation requires commitment and SMEs face an uphill staffing challenge.

Respondents cited a lack of digital skillsets, incompatibility between old and new systems and expensive implementation as major challenges for digital adoption.

This is especially true among the medium-sized SMEs as they have already embarked on digitalisation and may find it more challenging to expand their efforts across the organisation.

Figure 6: Challenges of digital adoption to be expected by SMEs. Source: UOB SME Outlook Study 2022

Smaller SMEs with less than S$10 million turnover tend to look for digitalisation funding support through tax incentives and rebates (39 per cent) as well as easier access to funding or grants (41 per cent).

Medium-sized SMEs, on the other hand, look for opportunities to collaborate with industry bodies, government-linked companies and large businesses (40 per cent). Other expectations from medium-sized SMEs include finding connections to the right technology and solution providers (38 per cent) as well as gaining access to business analytics and relevant insights (36 per cent).

Right partner essential for digitalisation journey

Digitalisation is a journey and having the right partner is essential to maximising its benefits.

One in two SMEs surveyed believe that banks have a vital role to play, citing that they can provide insights to support SMEs in their digital journey (51 per cent) and to be a facilitator with the government (49 per cent). This assistance is essential in promoting sustainable growth for SMEs.

UOB connects businesses to digital transformation initiatives that enable business efficiency and growth, which is in line with the new normal.

For instance, UOB BizSmart is an integrated business management solution for small businesses across the region, with services ranging from account and pay-roll management to e-commerce, provided by industry partners curated by the Bank.

SMEs can also tap on instant online account opening and onboarding services, with a smooth client experience including straight-through service for aspects like loan applications. The digital authentication of transactions, or the use of product applications using digital signatures (Sign with Singpass), ensures transaction security for SMEs.

Beyond financing, we also offer digital general insurance for SMEs across ASEAN. Companies can access information readily at their convenience and are guided to pick the right plan. Essentially, there is transparency in pricing for different industries and the insurance policy can be stored and retrieved digitally.

1The UOB SME Outlook Study 2022 was a survey conducted from late December 2021 to early January 2022, among 800 local SMEs with revenue of less than S$100 million. The study aimed to understand the business outlook and key expectations among SMEs in Singapore.

Important notes and disclaimers

This article shall not be copied or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Find out how we can help your business expand across ASEAN Get in touch